Managing money is at the root of all major decisions in business, and financing plays a vital role in accessing the capital needed to propel a business forward. It provides companies with the necessary funds to start, operate, and expand their operations. How effectively business financing is managed during periods of high-interest rates can make or break a company.

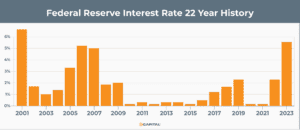

On July 26, 2023, the Federal Reserve raised the interest rate by 0.25% to as much as 5.5%, the highest level in 22 years. This move was initiated as a continuing attempt to curb persistent inflation in the U.S. economy. However, some analysts anticipate yet another rate increase before the end of the year to cool demand and stabilize prices. With each rise in interest rates (and there have been many since the spring of 2022), businesses with company credit cards and existing loans suffer higher interest payments. For most businesses, the outcome is less net income and larger overhead costs. For many, it also results in restricted credit as traditional lenders become more cautious.

As business financing is vital to sustain operations and fuel growth, companies must find ways to leverage credit to their best advantage despite adverse conditions. Learn how to effectively manage business financing during the nation’s highest interest rate period in over 22 years.

Interest rates impact on financing

Central banks typically use interest rates as a tool to manage inflation. Since spring 2022, the US Federal Reserve has increased rates 11 times. The latest increase was on July 26th when the Fed raised rates a quarter percentage point to a target range of 5.25%-5.5%.

Financing challenges have intensified as traditional business loans become harder to obtain and maintain due to banks restricting lending to companies with underperforming business levels and poor credit histories. Businesses that flourished in a low-interest rate economy following the great recession of 2008/2009 are now struggling with high debt servicing costs. These higher costs increase the business’s cash outflows and negatively impact significant financial metrics such as leverage ratios.

For businesses already struggling with rising payroll and supply costs, the addition of increasing debt payments is creating a perfect storm, often resulting in financial distress. In this economic environment, businesses must find a flexible financing solution to fulfill their working capital needs with repayment schedules tailored to meet the company’s financial resources.

Where can businesses find flexible funding?

Fortunately, as traditional lenders are shrinking the credit market, alternative lenders are filling the gap, providing flexible funding solutions to help businesses access working capital without incurring further debt.

Alternative finance companies offer niche financing solutions custom-made for businesses pursuing growth opportunities, expansion strategies, or struggling to overcome financial distress. One such solution is invoice factoring – a cash flow enhancement strategy ideal for companies needing fast, reliable access to working capital without the liability of rising interest rates. Let’s explore invoice factoring and how it’s become a go-to business financing strategy across multiple industries.

Invoice factoring: a non-debt solution

Invoice factoring is an alternative financing solution for B2B businesses that regularly issue invoice receivables to creditworthy customers. This financing method turns outstanding accounts receivables into immediate cash. Invoice factoring is the selling of invoice receivables at a discount in exchange for immediate payment. It is designed to unlock the money your business has already earned so you can access working capital within hours instead of waiting 30 or 60 days for your customers to pay.

How effectively business financing is managed during periods of high-interest rates can make or break a company. Because invoice factoring is the selling of assets (invoice receivables), it does not incur debt, and costs are more controlled. Fees for advanced funds are based on a percentage of the invoice face value, not a formula that demands regular payment based on the loan principal amount and interest rate spread over the loan term. The result is a financing solution with payment terms that keeps pace with business output. This means fees are reduced if business slows and the volume or amount of invoice receivables decreases. Conversely, if the business grows, funding increases, but the factoring fee remains constant at the same percentage rate as previously agreed in the factoring contract. The cost of financing is associated with the volume of business as opposed to monthly loan servicing costs, which can increase substantially over time as interest rates continue to elevate.

A growing number of business owners and financial executives favor invoice factoring as an easy-to-manage funding solution with multiple advantages. Financial planning is simplified as invoice factoring delivers immediate funds, making determining cash flow projections easy.

Here are additional benefits of invoice factoring:

A different approach to credit qualification: Traditional lenders base loan approvals on the borrowing company’s business performance levels and credit score. This approach minimizes the lender’s risk but restricts most SMEs from qualifying for credit. Alternative lenders take an entirely different approach to qualify businesses for invoice factoring. These lenders integrate technology-driven methodologies to quickly access vast databases and assess the credit strength of the company’s customer base – the debtors responsible for invoice payments. This method provides a more equitable analysis, helping to qualify companies with creditworthy customers despite having underperforming business levels and less-than-perfect credit records.

Fast access to working capital: Advanced funds, typically 80-90% of the invoice value, are transferred directly to the company’s cash account within hours of the invoice being submitted and verified. The remaining 10-20% is held in reserve until the customer pays the invoice. Once the invoice is fully paid, the reserve amount is rebated, less the factoring fee and any additional costs as stated in the factoring agreement.

No impact on your credit score: Invoice factoring is not a loan it is the selling of an asset. No debt is incurred, and therefore, there is no impact on your credit score.

Funding keeps pace with business growth: The more invoices your business generates to creditworthy customers, the more funds become available.

Full transparency and accountability: Tech-enabled invoice factoring companies provide a robust online account management portal to allow client businesses 24/7 access to real-time data. Monitor account balances, track transactions, and view credit limits to help keep a watchful eye on your business’s financial health.

Streamlined efficiencies: Dedicated account managers help onboard new clients, streamline services, and clear the tracks of any issues that may impact regular funding.

Credit protection: Invoice factoring companies have experienced credit teams and managers to help manage enhanced risk management practices. Their expertise and access to expansive databases provide the resources to assist in identifying potential risks associated with new business customers and help to avoid bad debt.

Operational agility: Businesses with easy access to working capital have more financial flexibility to adapt to changing economic conditions. Further, when new business opportunities develop, invoice factoring’s flexibility allows credit limits to increase as the client business’s size or volume of invoices grows.

Conclusion

Financing is vital in accessing the capital needed to propel a business forward. As interest rates continue to climb, traditional bank financing has become an escalating and challenging burden for businesses. Each interest rate hike increases the cost of borrowing money, jeopardizing the financial security of companies requiring business financing. How effectively business financing is managed during periods of high-interest rates can make or break a company.

As banks raise rates, lock down lending standards, and restrict access to credit, alternative lenders are moving in the opposite direction to increase access to working capital. Leveraging business assets and the credit strength of a company’s customer base, leading alternative lenders can extend credit to businesses in multiple industries via innovative financing options such as invoice factoring.

Invoice factoring is a non-debt financing solution that allows businesses to leverage the value of outstanding invoices to unlock the cash needed to maintain stability or chart a path toward recovery. In this environment of low growth and high-interest rates, invoice factoring provides fast access to working capital and additional benefits to enhance sustainability. Easy to qualify for and simple to manage, invoice factoring provides enhanced credit protection and operational agility to support financial stability and growth.

Many SMEs now consider invoice factoring as their preferred funding solution to cost effectively manage business financing during the highest interest rates in 22 years.

Key Takeaways

- Companies must find ways to leverage credit to their best advantage despite the highest interest rates in 22 years.

- For businesses already struggling with rising payroll and supply costs, the addition of increasing debt payments often results in financial distress.

- Businesses must find a flexible financing solution to fulfill their working capital needs with repayment schedules tailored to meet the company’s financial resources.

- Invoice factoring is a non-debt financing solution.

- A growing number of business owners and financial executives favor invoice factoring to cost effectively manage business financing.

ABOUT eCapital

At eCapital, we accelerate business growth by delivering fast, flexible access to capital through cutting-edge technology and deep industry insight.

Across North America and the U.K., we’ve redefined how small and medium-sized businesses access funding—eliminating friction, speeding approvals, and empowering clients with access to the capital they need to move forward. With the capacity to fund facilities from $5 million to $250 million, we support a wide range of business needs at every stage.

With a powerful blend of innovation, scalability, and personalized service, we’re not just a funding provider, we’re a strategic partner built for what’s next.