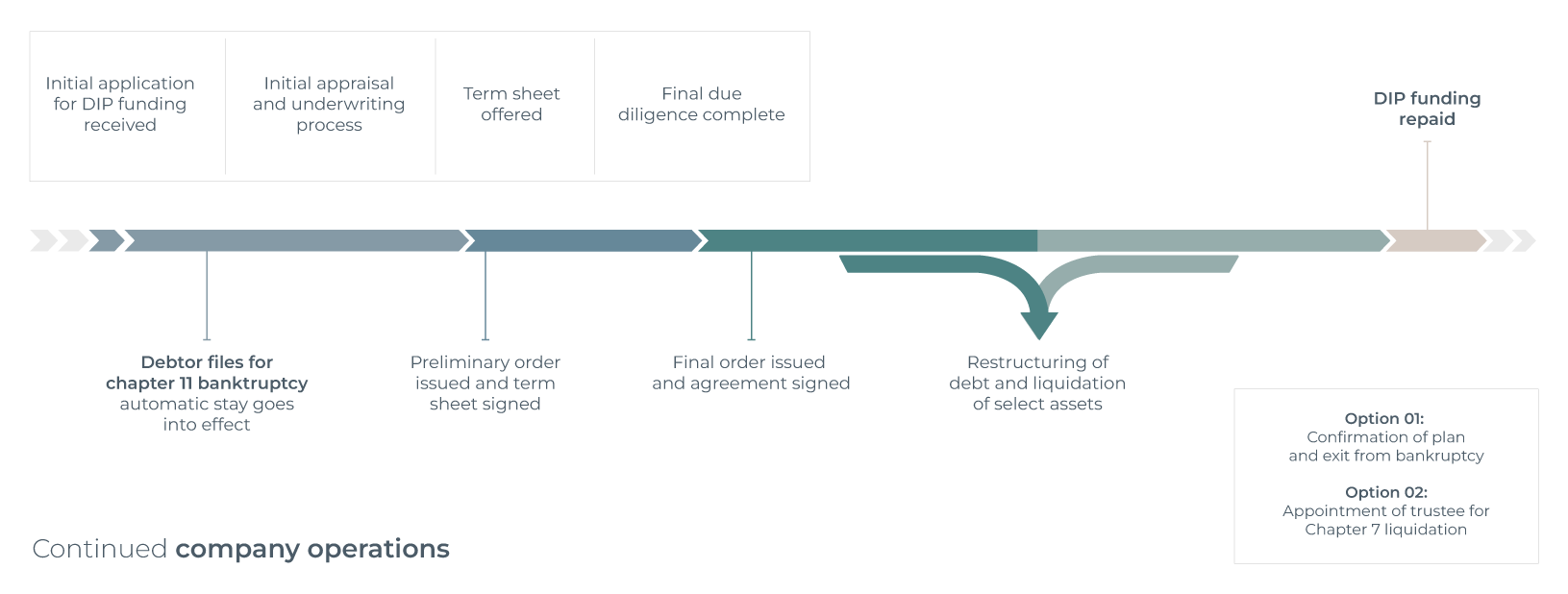

Businesses in financial distress typically find that sources of traditional funding shrink when they need it the most. As a b. . .

DEBTOR-IN-POSSESSION

Power your DIP turnaround with purpose-built funding

DIP financing is a powerful tool that can help your business get back on track during a formal restructuring process.