TL;DR:

Expanding fleet size can increase revenue and long-term growth potential, but it also significantly increases costs, operational complexity, and cash flow pressure. Before financing another truck, trucking companies should carefully evaluate profitability, freight demand, monthly affordability, and risk exposure through detailed financial analysis and “what if” scenarios. Strong cash flow management, realistic planning, and financing strategies like freight factoring can help growing fleets manage the increased financial demands of expansion more sustainably.

Many trucking company owners associate having more trucks with greater success, especially in the early stages of growth. For a small trucking company, adding another truck is a major operational and financial milestone. For an owner/operator, adding a second truck often marks the transition from being a contractor to managing a growing business. However, the investment involved is a significant turning point for a trucking company and deserves extensive consideration.

Fleet expansion increases revenue potential, but also significantly expands costs, risk exposure, staffing demands, and cash flow requirements. For most small trucking companies, acquiring additional working equipment typically requires financing for a semi-truck. Trucking is a capital-intensive and competitive industry with slow-paying customers. Before taking on additional equipment debt, carefully evaluate whether projected freight volume, cash flow stability, and operating margins can comfortably support the investment.

This article explores the strategic, operational, and financial considerations trucking company owners should evaluate before using financing for a semi-truck to expand operations.

Why expand operations?

Owner-operators often hope that acquiring a second or third truck will help them transition from simply driving for income to building a scalable trucking business. Small trucking companies expect fleet expansion to generate increased revenue, operational leverage, and long-term financial stability.

A well-run trucking company can significantly increase annual net income by expanding to two or three trucks – but profit does not automatically double or triple. The greatest financial gains typically come when all trucks are consistently utilized, costs are controlled, and cash flow is managed effectively.

Risk vs reward

The decision whether to expand through financing for a semi-truck should be the result of a “risk vs reward” assessment. It involves analyzing available information, preparing for potential problems, and determining that the potential benefits outweigh the potential downsides.

Follow these three steps:

- Begin with an Additional Truck Expansion Checklist to assess your trucking company’s readiness to take on additional equipment, operating costs, and operational complexity.

- Assess the financial and operational performance indicators that help determine whether an additional truck can generate sustainable revenue and profitable growth.

- Revenue per mile: Estimate how much income each truck can generate per mile based on freight rates, lanes, and mileage.

- Cost per mile (CPM): Use a customized CPM calculator to ensure all fixed and variable operating expenses are accounted for.

- Truck utilization: Analyze historical performance to determine how many miles are revenue-generating versus deadhead or idle time.

- Freight market conditions: Monitor spot and contract rates, seasonal demand, economic trends, fuel prices, and industry capacity to assess whether freight demand is strong enough to keep multiple trucks moving consistently with minimal downtime.

- Expanding operations should not depend solely on best-case projections. Use the CPM calculator to conduct “what if” scenarios and evaluate how changes in operating conditions could impact profitability and cash flow before committing to another truck.

The goal is to determine whether the business can remain profitable and maintain healthy cash flow even when conditions become less favorable.

- Top of Form

- Bottom of Form

What can you afford each month?

Determining what your company can afford each month is the next step in determining whether financing for a semi-truck is financially sustainable for your business. Following steps 2 and 3 above will help answer this question.

Use the following information to guide “what if” scenarios:

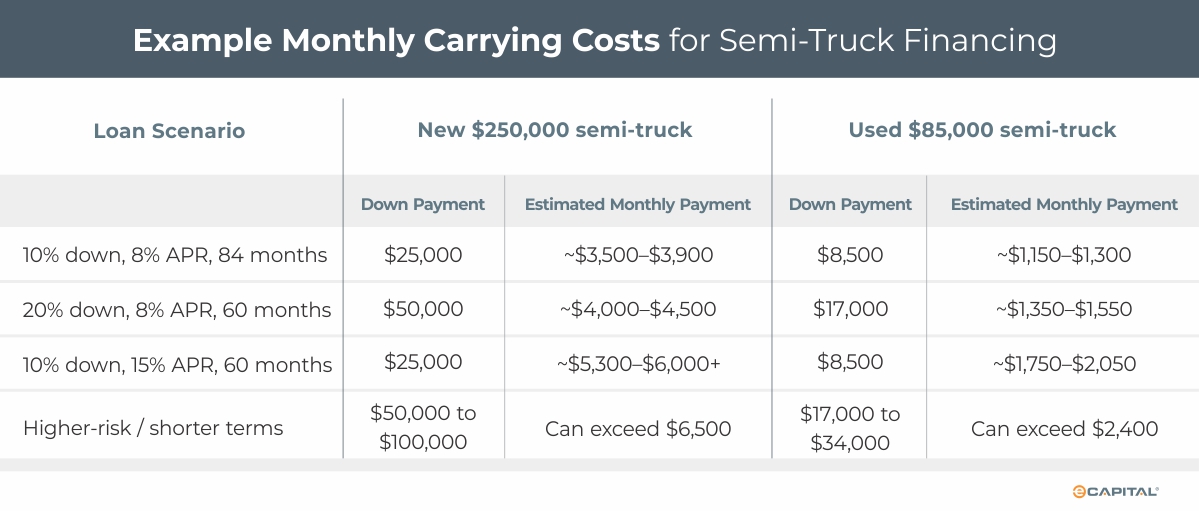

Cost of a new commercial semi-truck: Typically, costs range from approximately $130,000 to $300,000+ USD, depending on the truck type, configuration, sleeper size, engine, and technology package.

Cost for a used commercial semi-truck: These costs range from $20,000 to $120,000+ USD, depending on the truck’s age, mileage, condition, engine, sleeper configuration, and maintenance history. Most well-maintained late-model highway trucks fall within the $50,000 to $100,000 range.

Down payments: When using financing for a semi-truck, the typical down payment is between 10% and 30% of the truck’s purchase price. The exact amount of the down payment depends on factors such as credit score, time in business, truck age, operating history, and lender requirements.

For example, financing an $85,000 truck with a 20% down payment would require a $17,000 down payment, with the lender financing the remaining $68,000 balance.

Monthly payments: This is one of the most important factors to evaluate when considering financing for a semi-truck and determining whether expansion is financially sustainable. Financing terms typically range from 24 to 84 months, with interest rates varying widely based on credit profile, time in business, truck age, mileage, and lender risk assessment. Lower monthly payments may improve short-term cash flow, but longer loan terms can increase total financing costs over time.

Before you start shopping for trucks, calculate what you can afford each month – that way, you know which equipment option fits your budget.

Before you start shopping for trucks, calculate what you can afford each month – that way, you know which equipment option fits your budget.

Credit requirements for equipment acquisition

Small trucking companies applying for traditional financing for a semi-truck, or a leasing agreement, are typically evaluated based on:

- The owner’s personal credit profile: Owners with a credit score lower than 650 may qualify with larger down payments or higher interest rates.

- Business financial strength: Lenders want to see evidence of sufficient revenue and cash flow stability to support the investment.

- Trucking experience: Traditional lenders typically prefer trucking companies with at least 1–2 years of operating history.

- The overall risk of the transaction: Lenders assess the truck’s cost, age, condition, reliability, expected lifespan, and earning potential to determine whether the financing request presents an acceptable level of risk.

- Personal guarantee: Many small trucking company owners are required to personally guarantee the loan or lease.

While qualification requirements vary by lender, most traditional financing providers look for evidence that the business can reliably manage debt and operate profitably.

How freight factoring strengthens a financing application

Freight factoring accelerates freight bill payments. Using this strategic cash flow strategy improves working capital stability, increases liquidity, and can strengthen a trucking company’s financing application by demonstrating a stronger financial profile.

Key ways freight factoring supports a financing application include:

- Improved cash flow consistency: Factoring converts invoices into immediate cash rather than waiting 30–60 days for broker or shipper payments. Consistent cash flow provides lenders with greater confidence in the business’s ability to meet loan payment obligations.

- Strengthens bank balances: Faster access to receivables can improve average cash balances and reduce overdrafts or cash shortages that may negatively affect financing approval.

- Supports working capital stability: Freight factoring helps reduce the cash flow gaps that commonly strain growing fleets. Lenders want to see that the business can consistently cover fuel, insurance, payroll, maintenance, and loan payments.

Growing pains

Adding trucks increases revenue potential, but it also introduces growing pains – increased operational complexity, fixed expenses, and financial risk. Without strong operational controls, scaling can expose weaknesses that were less visible in a smaller operation.

Cash flow gaps are generally the dominant constraint, often becoming the primary reason profitable fleets fail. Each additional truck introduces significant costs – fuel, payroll, repairs, and insurance must often be paid weekly, while freight invoices may not be collected for 30 to 60 days. As fleets grow, this timing gap widens significantly. A company may appear successful based on truck count or gross revenue while simultaneously struggling with liquidity and rising debt obligations. Freight factoring is a proven mainstream financing strategy to accelerate cash flow, stabilize financial structures, and support financing for a semi-truck.

Conclusion

Expanding from one truck to two or three can create meaningful opportunities for revenue growth, operational leverage, and long-term business development. Still, it also introduces significantly greater financial and operational responsibility.

Successful fleet expansion requires more than simply acquiring additional equipment. It requires disciplined cash flow management, realistic profitability analysis, careful risk assessment, and a financing structure capable of supporting growth through changing market conditions. Trucking companies that approach expansion strategically, closely monitor key performance metrics, and maintain strong working capital stability are better positioned to grow sustainably while avoiding the financial strain that often accompanies scaling.

Ultimately, the decision to acquire a second or third truck should be based on a “risk vs. reward” assessment. The key question is whether the company can maintain cash flow stability and operational efficiency while preserving consistent customer service and increasing profitability through fleet growth.

Contact us to evaluate financing and cash flow strategies designed to help growing fleets scale with confidence.

Key Takeaways

- Fleet expansion increases revenue potential, but also significantly expands costs, risk exposure, staffing demands, and cash flow requirements.

- Before taking on additional equipment debt, carefully evaluate whether projected freight volume, cash flow stability, and operating margins can comfortably support the investment.

- Conduct a “risk vs reward” assessment and “what if” scenarios to evaluate how changes in operating conditions could impact profitability and cash flow before committing to another truck.

- The key question is whether the company can maintain cash flow stability and operational efficiency while preserving consistent customer service and increased profitability through fleet growth.

ABOUT eCapital

At eCapital, we accelerate business growth by delivering fast, flexible access to capital through cutting-edge technology and deep industry insight.

Across North America and the U.K., we’ve redefined how small and medium-sized businesses access funding—eliminating friction, speeding approvals, and empowering clients with access to the capital they need to move forward. With the capacity to fund facilities from $5 million to $250 million, we support a wide range of business needs at every stage.

With a powerful blend of innovation, scalability, and personalized service, we’re not just a funding provider, we’re a strategic partner built for what’s next.