Most businesses rely on external financing to support their day-to-day operations. And in every situation, lenders will require assurances that they will be repaid in a timely manner. These assurances often take the form of financial covenants that outline expectations up front and then enable the lender to monitor compliance over the life of the loan.

In the case of asset-based lending (ABL financing) or any form of credit secured by company assets, compliance typically includes monitoring of a borrowing base. The borrowing base is determined at the start of the lending process and must be constantly maintained throughout the loan term.

This article provides an explanation of borrowing base and how to calculate it. It further delves into what it takes to manage it, the importance of borrowing base to maintain business financing, and why it will become even more critical in 2024. Finally, we’ll look at asset-based loans that don’t require borrowing base monitoring and the lenders that provide.

What is a borrowing base?

A borrowing base is the amount of credit a lender will loan based on the appraised value of the assets they agree to use as security. Typical asset types used as collateral for ABL financing include accounts receivable, inventory, real estate, machinery, and equipment.

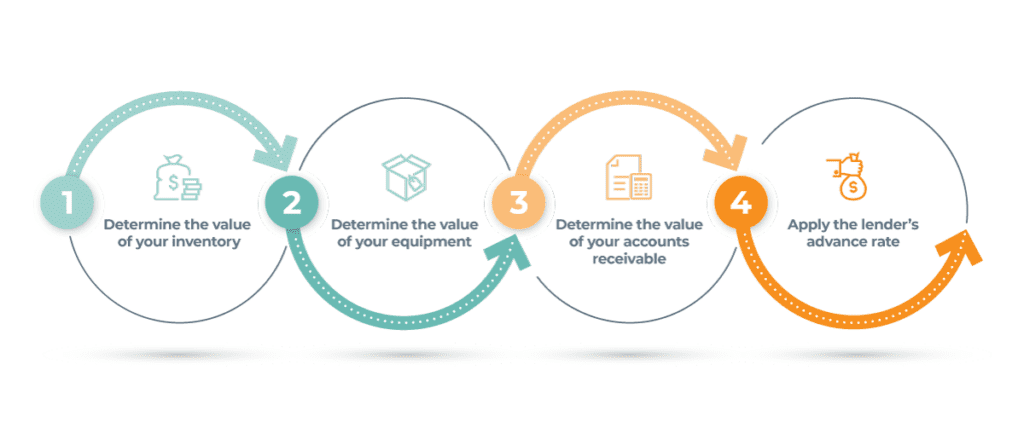

How to calculate a borrowing base?

Generally speaking, no lender will advance 100% of the value of your collateral. Instead, lenders apply an advance rate to determine how much funding your collateral will secure. The advance rate provides the lender with a cushion of protection in case the value of the collateral declines or the borrower defaults on the loan and the collateral needs to be liquidated quickly.

The formula for calculating a borrowing base is very simple:

Collateral Value x Advance Rate = Borrowing Base

Example: $1,000,000 (Collateral Value) x 75% (Advance Rate) = $750,000 (Borrowing Base)

NOTE: The advance rate is determined by the asset type used as collateral and the lender’s appetite for risk. Depending on these variables, advance rates typically range from 65% to 90% of the asset’s collateral value. 75% represents a common advance rate on the appraised collateral value for machinery, equipment, or real estate.

What does it take to manage your borrowing base?

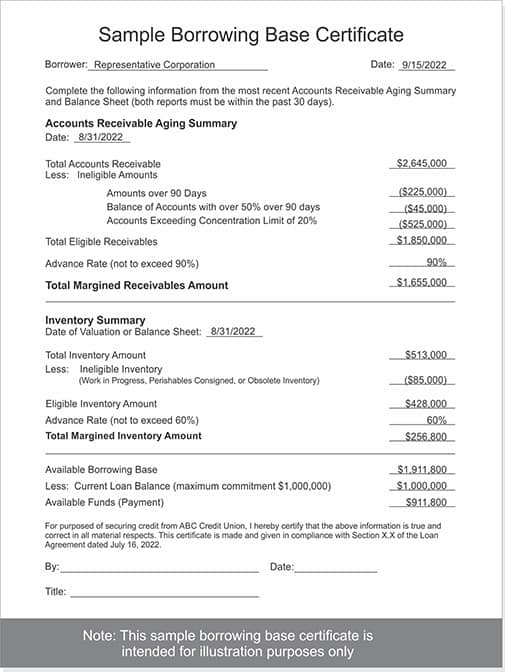

How often you will need to calculate your borrowing base and file a borrowing base certificate with your commercial lender will be defined in the terms of your loan agreement. Terms vary per agreement but may require the borrower to report monthly, weekly, bi-weekly, a few times each week, or even daily.

The bulk of work involved is not in performing the calculation – it is in determining the current equity of the collateral each time the calculation is to be made. As market conditions, collateral conditions, interest rates, and balances owed on existing loans change, so does the collateral’s equity.

Businesses will likely need to invest in staff, technology, or both to continually monitor their borrowing base. The work required can take up one-third or more of a controller’s time to accurately prepare the necessary documentation in a timely fashion.

Why is borrowing base critical to your business financing?

Business lines of credit and other forms of business financing are generally governed by financial covenants. These stipulations protect the lender by requiring the borrower to fulfill certain conditions or limit certain actions. A borrowing base is a commonly used covenant to ensure the borrower’s credit does not exceed the collateral value assigned to the loan. In most cases, if the reported borrowing base value falls below the current loan balance, the company may be required to repay the difference to the lender at once. This action is needed to satisfy the loan covenants and avoid violating credit agreements. As a result, efforts to maintain your company’s borrowing base can be critical to maintaining access to credit.

Why borrowing base will be even more critical in 2024

Economic conditions are continuing to batter businesses’ financial performance. 2024 will be a critical year for managing business financing. As the economy struggles to regain stability and growth, governments, lenders, and borrowers will diligently review financial conditions to identify and protect themselves from credit risk. Government regulators such as the Federal Reserve and the FDIC regularly examine banks to identify and address potential risks to the bank, its customers, and the financial system. Acting to satisfy government oversight and protect their stakeholders, banks are beginning to review their lending portfolios more diligently to assess risk exposure. Any borrower that has broken or is in danger of violating a loan covenant (such as the value of their borrowing base) or otherwise found likely to become a credit risk is in danger of facing credit restrictions or receiving a bank recall of credit.

And unfortunately, this can happen at any time! Through internal review processes, business owners may discover that their financials do not meet the covenant requirements, and immediate action may be demanded. To avoid this scenario, it pays to be proactive. Plan a set of actions before your credit line is reduced to zero. Start by investigating flexible financing options and alternative lenders that can keep your business running through unexpected financial challenges.

Not all collateral loans require borrowing base monitoring

Many alternative lenders now provide various business financing options free from borrowing base requirements. For example, eCapital offers equipment refinancing to truck company owners. This asset-based lending option provides a large influx of capital to a business without the need for monthly auditing of assets. However, invoice factoring is a more common form of asset-based lending without borrowing base monitoring. Utilizing this mainstream financing option is a growing trend as businesses discover the many advantages of getting paid immediately once a service is rendered and an invoice is issued.

Alternative lenders to the rescue

As many businesses will be confronted with the probability of facing credit restrictions, or worse, a credit recall from their bank, alternative lenders are positioned to be credit heroes with flexible, cost-effective, and available funding options.

Tech-enabled alternative lenders can access extensive databases and assess hundreds of credit-related data points to uncover credit strengths and asset insights that aren’t available to traditional lenders. Utilizing these strengths, alternative lenders can quickly restructure and transition a business from bank financing to a more dependable funding source.

Conclusion

Banks continuously monitor loan covenants for compliance throughout the life of the loan. Borrowing base is one of the more significant covenants banks will focus on. Further, their risk appetite can change dramatically from one quarter to the next, depending on changing conditions. Any sign of weakening financial performance that could indicate a potential loan default may be enough to prompt the bank to restrict or recall credit.

Businesses dependent on asset-based bank financing are well advised to be one step ahead of the bank and carefully monitor their borrowing base. If necessary, start communicating with alternative lenders to establish a backup financial strategy should a quick transition be required. With proper planning, alternative lenders can quickly and seamlessly transition a business to a more dependable and flexible financing structure without any funding gaps.

ABOUT eCapital

At eCapital, we accelerate business growth by delivering fast, flexible access to capital through cutting-edge technology and deep industry insight.

Across North America and the U.K., we’ve redefined how small and medium-sized businesses access funding—eliminating friction, speeding approvals, and empowering clients with access to the capital they need to move forward. With the capacity to fund facilities from $5 million to $250 million, we support a wide range of business needs at every stage.

With a powerful blend of innovation, scalability, and personalized service, we’re not just a funding provider, we’re a strategic partner built for what’s next.