Access to finance is one of the biggest challenges facing small businesses and start-ups. Many struggle to secure funding due to limited financial history, a lack of collateral, or an insufficient credit rating. Without adequate funding, business owners may find it difficult to invest in growth, innovation, or operational improvements.

Micro loans offer a practical solution, providing smaller amounts of capital with more accessible terms than traditional lending options. Whether for launching a new venture, purchasing equipment, or managing day-to-day expenses, micro loans play a vital role in supporting small business growth across the UK.

In this guide, we explore micro loans, how they work, and why they are a crucial funding option for businesses looking to scale.

What Are Micro Loans?

Micro loans are small, short-term loans designed to support the financial needs of start-ups, sole traders, and small businesses. Typically ranging from a few hundred to tens of thousands of pounds, these loans are particularly useful for businesses that may not qualify for traditional bank loans.

Key Features of Micro Loans:

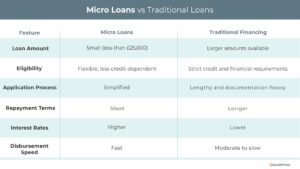

- Smaller Loan Amounts – Typically up to £100,000, making them ideal for modest funding needs.

- Flexible Eligibility – Available to new businesses, sole traders, and entrepreneurs from underrepresented backgrounds.

- Short Repayment Terms – Usually repaid within six months to five years.

- Accessible Providers: Offered by microfinance institutions, non-profits, and alternative lenders.

How Do Micro Loans Work?

- Application – Borrowers submit a loan application, often with fewer requirements than traditional business loans. Lenders may assess business plans, revenue projections, and community impact.

- Approval Process – Micro lenders evaluate a borrower’s repayment ability, considering factors such as trading history, financial projections, and industry sector.

- Disbursement – Once approved, funds are typically released quickly—sometimes within days.

- Repayment – Borrowers repay the loan in regular instalments, which may include interest and service fees.

Who Can Benefit from Micro Loans?

Micro loans are particularly useful for businesses and individuals who may struggle to access mainstream finance:

- Start-Ups – Entrepreneurs looking for capital to fund initial operations, inventory, or marketing.

- Small Business Owners – Businesses that require a small amount of funding for expansion or cash flow support.

- Sole Traders and Freelancers – Self-employed professionals needing financial support to invest in equipment, training, or materials.

- Social Enterprises and Community Projects – Businesses with a strong social impact may find micro loans more accessible than traditional funding routes.

Advantages of Micro Loans

- Accessible Funding

- Micro loans are designed for small businesses and start-ups that may be overlooked by traditional banks.

- Flexible Eligibility

- Fewer barriers to qualification compared to mainstream business loans, making them ideal for new or underrepresented entrepreneurs.

- Fast Disbursement

- Many micro lenders operate with quicker processing times, allowing businesses to access funds when needed.

- Supports Credit Building

- Repaying a micro loan on time can help businesses establish or improve their credit scores.

- Community-Focused Lending

- Many microfinance institutions prioritise social and economic impact, reinvesting in local businesses and entrepreneurs.

Challenges of Micro Loans

- Higher Interest Rates

- Due to the increased risk associated with lending to small businesses, interest rates may be higher than traditional loans.

- Limited Loan Amounts

- Micro loans are best suited for small-scale funding needs and may not provide sufficient capital for larger investments.

- Short Repayment Terms

- While shorter loan terms can reduce interest costs, they may put pressure on cash flow if repayments are not carefully managed.

- Lender Quality Varies

- Not all micro lenders operate with transparency; borrowers should carefully vet lenders to avoid inadequate financing, poorly structured facilities, or fraud. Look for a reputable lender by checking case studies, and the lender’s credentials.

Industries That Benefit from Micro Loans

- Retail and E-Commerce – Small retailers and online sellers use micro loans to stock inventory or enhance their online presence.

- Food and Beverage – Entrepreneurs launching cafés, food trucks, or catering services can benefit from this type of financing.

- Artisans and Craftspeople – Creative businesses often use micro loans to fund materials, equipment, and market stalls.

- Agriculture and Sustainable Businesses – Farmers and eco-friendly enterprises use micro loans to invest in sustainable practices.

- Service-Based Businesses – Sole traders, such as hairdressers, fitness trainers, and IT consultants, can use micro loans to grow their businesses.

Real-World Example: Micro Loans in Action

Scenario:

A budding entrepreneur in Manchester wants to start a mobile coffee van but lacks the funds to purchase equipment and stock.

Solution:

The entrepreneur secures a £20,000 micro loan from a community lender to cover the cost of a second-hand van, an espresso machine, and initial stock.

Outcome:

Within six months, the coffee business gains a loyal customer base, allowing the owner to repay the loan while reinvesting profits to expand the menu and secure more locations.

How to Choose the Right Micro Loan

- Research Lenders

- Look for reputable microfinance institutions, government-backed schemes, and ethical lenders.

- Understand Costs

- Review interest rates, fees, and repayment schedules to ensure the loan is affordable.

- Prepare a Business Plan

- Lenders may request details about how the funds will be used and projected revenue.

- Check Eligibility Criteria

- Ensure you meet the lender’s requirements before applying to improve your chances of approval.

The Future of Micro Loans

With advancements in financial technology (fintech), micro loans are becoming even more accessible. Online platforms and mobile banking have streamlined the application process, making it easier for small businesses across the UK to secure funding. As these innovations grow, micro loans will continue to play a crucial role in supporting start-ups, freelancers, and small business owners.

Conclusion

Micro loans are much more than just small-scale financing—they are a vital tool for economic empowerment, business growth, and job creation. Whether you’re a start-up needing initial capital, a sole trader looking to invest in equipment, or a small business managing cash flow, a micro loan can provide the boost you need to succeed.

Contact us today to explore micro loan options that suit your business needs.

Key Takeaways

- Start-ups and small businesses often struggle to access traditional funding due to a lack of financial history or collateral.

- Micro loans offer a flexible and accessible financing option, helping businesses cover operational costs, stock inventory, or invest in growth.

- These loans have lower qualification barriers and can be processed faster than conventional bank loans.

- Repaying a micro loan on time can help build business credit, increasing future borrowing opportunities.