A commercial property loan is an essential business financing tool to acquire, expand, or refinance commercial properties. It provides the necessary funds for companies to purchase and develop high-value properties, such as office space, retail units, warehouses, or other commercial real estate assets.

This blog explores commercial property loans, how they work, their benefits, and what businesses need to know to secure the right loan for their needs.

What Is a Commercial Property Loan?

A commercial property loan is a type of mortgage specifically designed for financing real estate used for business purposes. These loans are tailored for purchasing or refinancing properties such as offices, retail centres, industrial facilities, or multi-unit residential buildings.

Key Features of Commercial Property Loans:

- Secured by Property: The purchased property acts as collateral for the loan.

- Larger Loan Amounts: Designed to support high-value property purchases.

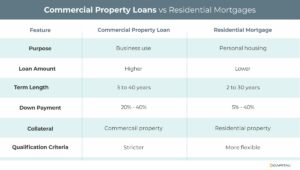

- Flexible Terms: Loan terms typically range from 5-year to 40-year amortization periods.

- Interest Options: Fixed or variable interest rates depending on the lender and market conditions.

How Do Commercial Property Loans Work?

- Loan Application: Businesses apply for a loan, providing financial documentation and details about the property.

- Assessment: Lenders evaluate the borrower’s creditworthiness, business income, and the property’s value and income potential.

- Approval: The loan is approved based on the borrower’s financial stability and the property’s projected ability to generate revenue.

- Disbursement: The lender provides the funds, typically covering a percentage (e.g., up to 80%) of the property’s purchase price.

- Repayment: Borrowers repay the loan through regular instalments over the agreed term.

Types of Commercial Property Loans

- Traditional Commercial Mortgages

- Fixed-term loans for purchasing or refinancing commercial real estate.

- Government-Backed Loans

- Government finance and support programs may offer favourable lending terms and advice for small businesses.

- Bridge Loans

- Short-term financing to cover immediate needs until permanent financing is secured.

- Development Loans

- For constructing new commercial properties or significant renovations.

- Asset-Based Loans

- Short-term loans based on property value, often used for quick acquisitions.

Benefits of Commercial Property Loans

- Property Ownership

- Allows businesses to own their premises rather than renting, building equity over time.

- Stable Costs

- Fixed-rate loans provide predictable monthly payments, protecting against rising rental costs.

- Revenue Generation

- Commercial properties can generate rental income if leased to other businesses.

- Tax Advantages

- Interest payments and property depreciation may be tax-deductible, reducing the overall cost.

- Business Growth

- Owning commercial property can enhance credibility, provide space for expansion, and improve asset value.

Challenges of Commercial Property Loans

- Higher Deposit Requirements

- Commercial property loans typically require larger deposits, often ranging from 20%-40% of the property’s value.

- Stricter Qualification Criteria

- Lenders require strong credit scores, financial statements, and sometimes collateral beyond the property.

- Variable Costs

- Loans with adjustable interest rates can lead to fluctuating monthly payments.

- Maintenance and Repairs

- Property ownership includes ongoing costs for upkeep, insurance, and business rates.

- Longer Approval Process

- Commercial property loans involve extensive evaluation and longer approval timelines than residential mortgages.

Eligibility Requirements for Commercial Property Loans

- Business Financials

- Strong financial statements, including balance sheets, income statements, and cash flow projections.

- Creditworthiness

- Good personal and business credit scores to demonstrate reliability.

- Deposit

- Ability to provide the required deposit (often 20%-40%).

- Property Value and Purpose

- The property’s value and intended use must align with the loan terms.

- Debt-Service Coverage Ratio (DSCR)

- Lenders often require a DSCR of 1.25 or higher, indicating the property generates sufficient income to cover debt payments.

Tips for Securing a Commercial Property Loan

- Improve Your Credit

- Both personal and business credit scores impact loan eligibility. Ensure your credit is in good standing.

- Prepare Financial Documentation

- Provide accurate and detailed financial statements to demonstrate your business’s ability to repay the loan.

- Save for a Deposit

- Accumulate sufficient funds for the required deposit and associated costs.

- Research Loan Options

- Compare lenders, interest rates, and terms to find the best fit for your needs.

- Consult Experts

- Work with commercial real estate brokers, financial advisors, or loan officers to navigate the process effectively.

Real-World Example: Commercial Property Loan in Action

Scenario: A growing restaurant chain needs £800,000 to purchase a property for its newest location.

Solution: The business secures a government-backed loan covering 80% of the purchase price with a low-interest rate and a 25-year term.

Outcome: The restaurant opens its new location, reduces monthly costs compared to leasing, and builds equity in the property over time.

Conclusion

A commercial property loan is a powerful tool for businesses investing in real estate, expanding operations, or reducing overhead costs. While the process may seem complex, careful planning, research, and preparation can make securing a loan more manageable.

By owning commercial property, businesses gain stability, potential tax benefits, and the opportunity to grow their assets. If you’re considering a commercial property loan, consult with trusted lenders and financial advisors to ensure the loan aligns with your business goals. With the right financing, your company can thrive in the commercial real estate sector with terms tailored to meet your business needs.

Contact us – our experienced team of financial specialists is available to consult, advise, and administer effective financing solutions to meet your business goals.

Key Takeaways

- A commercial property loan provides the necessary funds for companies to acquire and develop high-value properties.

- These loans are tailored for purchasing or refinancing properties such as offices, retail centres, industrial facilities, or multi-unit residential buildings.

- Careful planning, research, and preparation can make securing a loan more manageable.